On the Spot: A Busy Data Docket Awaits

Market run-through

The markets continued to digest the recent central bank meetings this week whilst keeping a wary eye out for further developments in the Middle East. It felt like every central banker going took their turn at the speakers’ rostrum during the week. Did we learn anything new? Probably not. The mantra of higher for longer is still being repeated by Jerome Powell and most of his companions, despite the American economy possibly showing the first signs of an impending recession, with weekly jobless claims rising for the last seven weeks. The commitment of the Bank of England to a similar policy seems slightly less unanimous, especially after its Chief Economist, Huw Pill, hinted that his view was that interest rates might drop before the next General Election. In his defence, the government may wait till Spring 2025 before going to the country.

Towards the end of the week, possibly the most critical indicator that rates are going to stay high, if not go higher, was seen when a US Bond auction had a lukewarm reception and, in doing so, pushed yields higher, helping the US dollar to regain some poise in what is typically a challenging month for it. Fans of the greenback will undoubtedly be watching how the US Bond market performs this week. Tomorrow sees the release of the latest US inflation numbers, which are expected to show further colling and could well set the tone for the dollar for the rest of the week. Inflation is also on the ECB’s calendar this week, with the Eurozone’s CPI for October released on Friday. The coming week could also be pivotal for the Bank of England and sterling with the release of employment and wage data on Tuesday and inflation on Thursday. So, all to play for in what should be an exciting week, and of course, we are always here to guide you through these challenging times.

Richard Matthews, Head of FX and Payment Partnerships

Behind the desk

Last week we saw huge price swings in two of the largest cryptocurrencies, bitcoin (BTC) and Ethereum’s ether (ETH). This extended period of high volatility comes at a time when BTC and ETH prices have been surging amid institutional interest in crypto ETFs. BTC soared through $36,000, and $37,000 for the first time since May 2022, almost reaching $38,000 before taking a sharp retracement. The big talking point, however, has been ETH after spiking 9% on news of an iShares Ethereum Trust. This price surge has helped ETH gain back some market dominance against BTC, which has consistently outperformed ETH over recent months.

According to a 19b-4 filing made on Thursday afternoon, BlackRock is confirmed to be working on a spot ether ETF. BlackRock registered a new corporate entity in the U.S. state of Delaware, where many corporations set up shop. This doesn’t come as a surprise as the asset manager has shown increasing interest in crypto over the past months and is currently awaiting a decision on its BTC ETF application.

Another lively topic of debate that has arisen is that of gas fees, posing questions surrounding the scalability of coins such as ETH and BTC. As prices continue to rise, there is a greater demand for blockspace, resulting in higher transaction fees. On the desk, we experienced longer wait times when sending and receiving crypto, alongside higher transaction fees. This was universal, with reports of gas fees as high as $220 for high-priority transactions on ETH. BTC, however, seemed to be all around cheaper, with an average of $9 for high-priority transactions. This may seem low in comparison, but BTC fees haven’t been this high since May.

This rise in fees has definitely prompted a shift to other blockchains in order to take advantage of the cheaper transaction rates. For example, on the desk, there were increased volumes in TRC and MATIC chain transactions. The flow at ONE has increased, not only in BTC and ETH but across other alts as well. It is definitely an exciting time, with price action reflecting a market that is smiling upon crypto again.

Alex-Desmond Brathwaite, Senior Trader

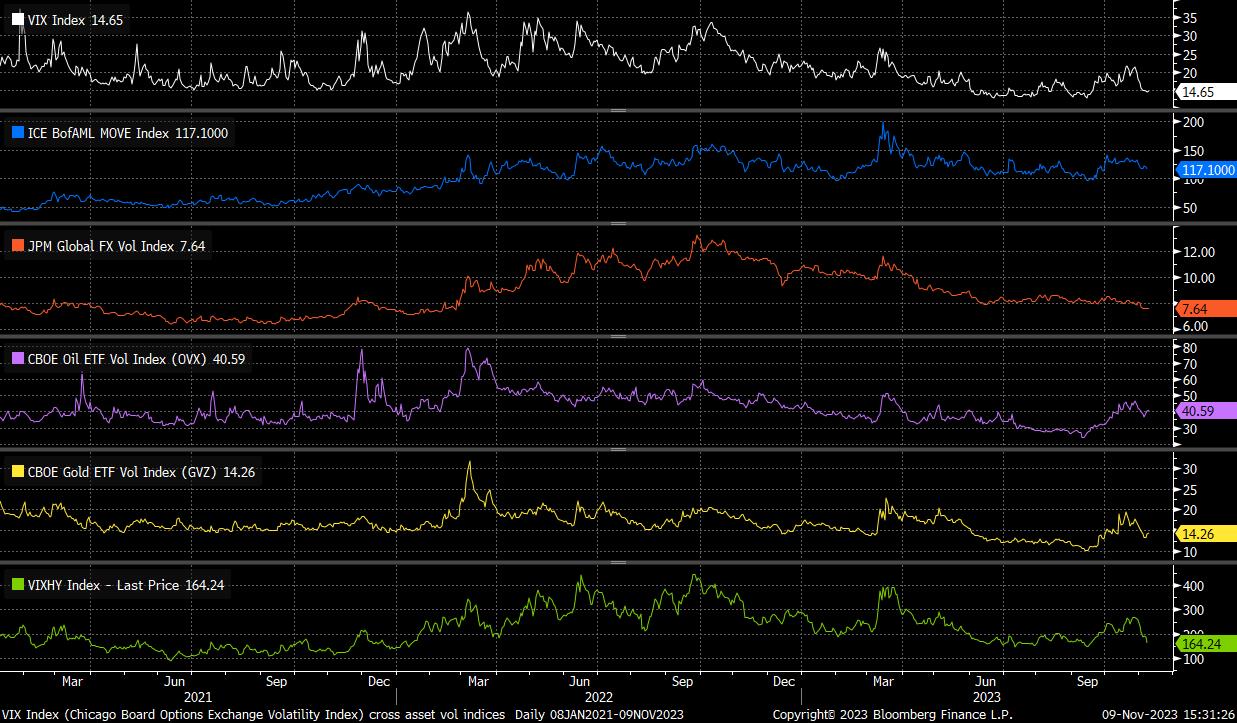

Chart of the week

It’s been a relatively quiet week for financial markets, with data and news flow both lacking amid a quiet economic calendar, and with a plethora of Fedspeak largely being ignored, with all policymakers seemingly reading from the same script, again emphasising a data-dependent bias to tighten further if necessary. Unsurprisingly, implied volatility has pulled back significantly across all asset classes, with the VIX back under the 15 handle, JPM’s FX volatility index touching new 18-month lows, and implieds seeing a similar fall elsewhere. Clearly, this poses the question as to whether financial markets may have become a touch too complacent – particularly with geopolitical tensions remaining elevated, and with a busy data docket coming up next week, including the latest UK and US inflation figures.

Michael Brown, Market Analyst at Pepperstone

The views contained herein are not to be taken as a recommendation or advice. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. It is very important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on ONE’s website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. It should be noted that investment involves risks, the value of investments may fluctuate in accordance with market conditions and investors may not get back the full amount invested.

Not all ONE services may be available to UK customers.